4 ways to cut your tax bill in retirement

Entering retirement can require a series of adjustments from how you spend your time to how you allocate your income. Retirement also has a direct effect on your taxes, providing access to valuable tax benefits you may not realize. Here are four lesser-known tax breaks you could be eligible for if you are planning to retire in 2023.

1. Higher Standard Deductions and Income Thresholds

More income may be exempt from taxes during retirement due to higher standard deductions and income thresholds.

In 2023, taxpayers aged 65 and over can take an extra $1500 standard deduction ($3000 for married couples filing jointly). That is in addition to the regular standard deduction of $13,850 for single filers and $27,700 for married couples.

This extra deduction does not apply if you itemize. If you or your spouse recently turned 65, you may want to calculate your taxes using both itemized and standard deduction formulas to determine which is more favorable. Many retirees find it no longer makes sense to itemize in light of the added deduction.

In addition to a larger standard deduction, higher income thresholds mean that some taxpayers over 65 do not have to file returns. Single taxpayers under 65 must file if they make at least $12,950 in 2022, but if they are 65 or over by the end of 2023, the amount increases to $14,700.

Married taxpayers where one spouse is over 65 do not have to file unless their income exceeds $23,700 (versus $25,900 for under 65 couples). If both are over 65, the threshold increases to $28,700.1

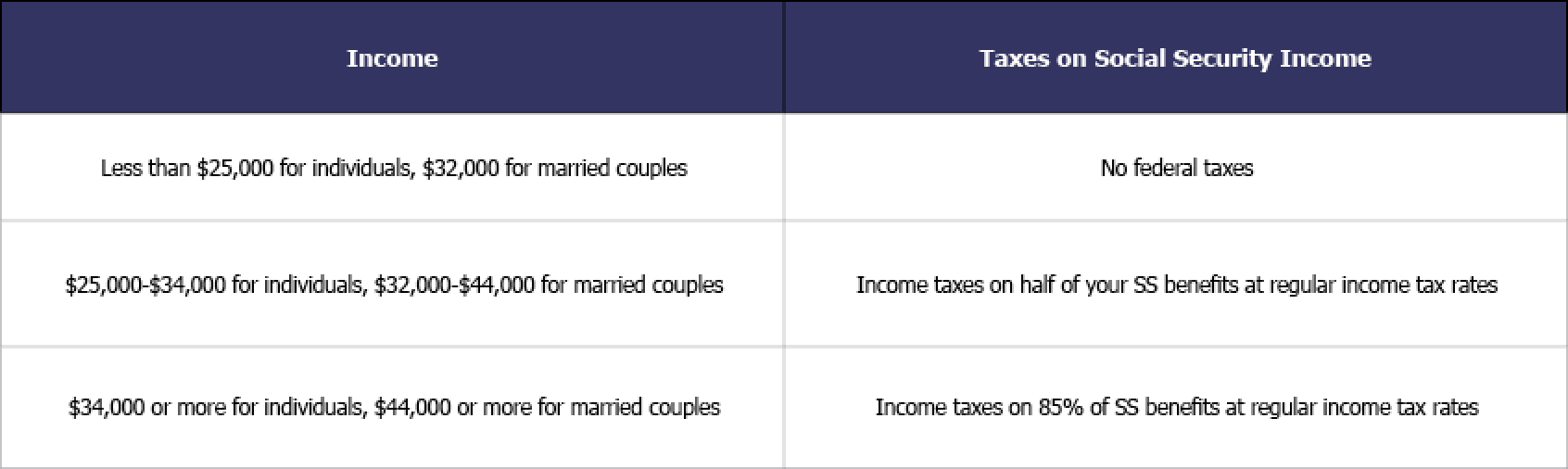

Bear in mind you may have to pay federal income taxes (and in some cases, state and local taxes) on your Social Security income if you have other substantial income sources. Here’s how your other income impacts Federal taxes on your Social Security income2:

In the below example, a married individual receives $20,000 in social security benefits, and their spouse earns $50,000/year.

The good news is, you do not have to pay FICA taxes on social security income.

You can pay these obligations with quarterly estimated tax payments or have a portion of your social security income withheld to meet them.

2. Deducting Medical Expenses

People often pay more for expenses like doctor visits, prescription drugs, tests and in-home care as they age, but some of these costs could lower your tax bill.

If your medical costs exceed 7.5% of your adjusted gross income, you can deduct them on your tax return as an itemized deduction.

Note that these expenses (combined with your other itemized deductions for state and local taxes, mortgage interest, and charitable gifts) would have to be larger than the standard deduction to make sense.

There are also some limits on the healthcare costs eligible for deduction. Personal expenses, such as vitamins or health club dues, generally do not count. However, you can deduct almost any payment to a medical professional including doctors, dentists, nurse practitioners, and therapists. Other qualifying expenses include:

Prescription drugs

Mental health expenses

Medical devices including glasses, dentures, and orthodontic appliances

Costs incurred while seeking medical treatment like parking fees at your doctor’s office

Health insurance premiums

Senior care costs such as in-home help or adult day services3

3. Tax Savings for Retirement Planning

In general, you can’t make tax-deferred contributions to retirement plans unless you have taxable income. However, you can still continue to save after you retire. For example, if your spouse continues to work, they can make contributions to savings plans. If you work part time or start a business that generates income, you can deduct contributions to IRAs, SEP-IRAs, SIMPLE 401(k)s, and other small business retirement plans from your earnings.

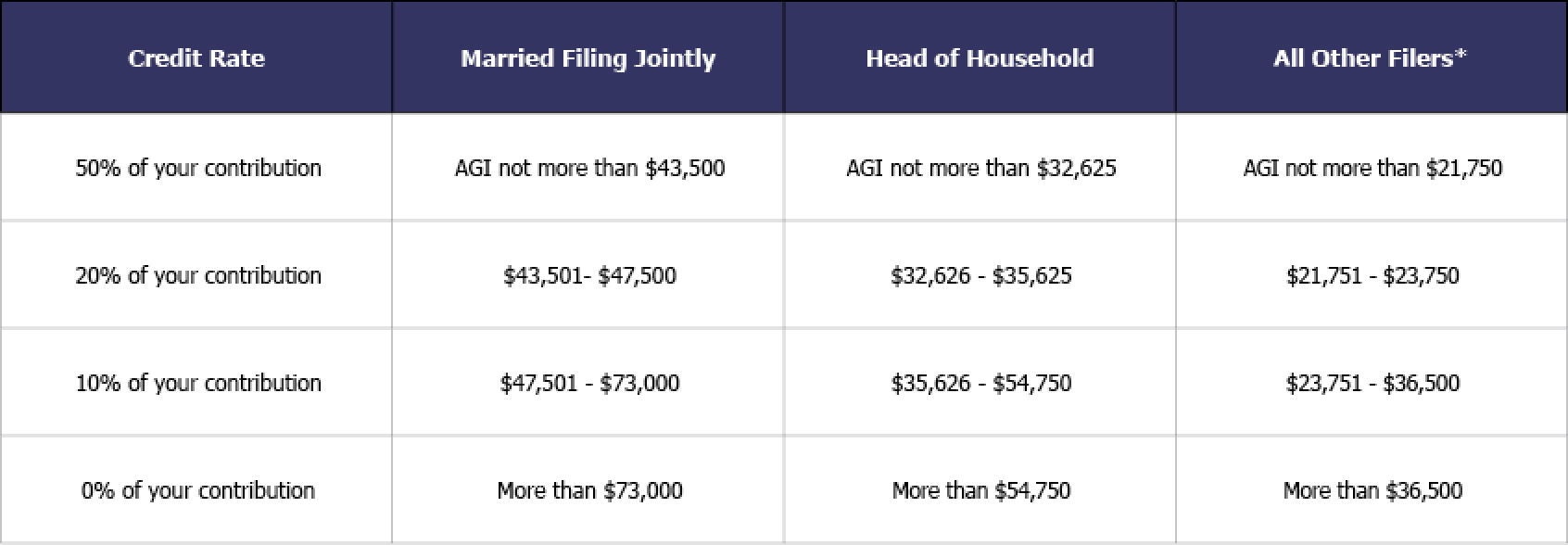

If your income is moderate after retirement and you continue to contribute to tax-deferred savings plans, you may be eligible for another tax-saving benefit: the Retirement Saver Credit. This program provides a tax credit that offsets up to half of your retirement plan contributions if you meet certain income limits.

For 2023, these limits are as follows:

*Single, married filing separately, or qualifying widow(er)

Source: “Retirement Savings Contributions Credit (Saver’s Credit)” IRS.gov, Retrieved March 20, 2023. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-savings-contributions-savers-credit

4. Small Business Credits

Many retirees continue to work in some fashion, either as consultants offering skills developed over a lifetime or in small businesses reflecting their passions. Of course, they have to pay taxes on their earned income but only after deducting a wide array of business expenses including:

Supplies including everything from paper to stamps to raw materials

Marketing and advertising expenses such as the cost of maintaining a website, printing business cards, or going to industry events and conferences

Travel to meet with clients and prospects

Home office expenses including a portion of home maintenance and utility costs

Business education and professional development

Employee wages and payments to independent contractors

Legal and accounting fees4

The rules about deducting business expenses can be tricky, so be sure to consult your tax professional if you have questions.

Also, many states have different tax laws and credits available to retirees. For an overview of what your state offers, visit your local tax authority’s website or check out this 50-state guide to retiree tax laws.

Make the Most of Your Retirement Income with Sound Tax Planning

Retirement brings with it a lot of changes including lifestyle, income, and taxes. Make sure you take proper advantage of the tax rules that apply to you once you retire or turn 65 and get the best value out of your income for the long run.

1“Dependents, Standard Deduction, and Filing Information,” IRS.gov, December 9, 2022. https://www.irs.gov/pub/irs-pdf/p501.pdf

2“Income Taxes And Your Social Security Benefit,” SSA.gov, Retrieved March 20, 2023. https://www.ssa.gov/benefits/retirement/planner/taxes.html

3“Medical and Dental Expenses,” IRS.gov, Retrieved March 20, 2023. https://www.irs.gov/taxtopics/tc502

4“Business Expenses 2022,” IRS.gov, Retrieved February 20, 2023. https://www.irs.gov/publications/p535

This article is provided for general informational purposes only. Neither New York Life Insurance Company, nor its agents, provides tax, legal, or accounting advice. Please consult your own tax, legal, or accounting professional before making any decisions.

SMRU #5500507.1 exp. 3/15/2025